There are three ways to do this. UK non resident tax can get complicated. For example, if a UK resident receives interest from a US bank account, that interest is normally exempt from US taxation (although there are some esoteric exceptions in addition to the ones mentioned above, but space precludes detailing them). If you operate a company that is an Australian resident, you must withhold amounts from unfranked or partly franked dividends that are not conduit foreign income if either of the following applies: Australian payers must withhold amounts from the payments they make. Caroline THIRIFAY Director of Investor Relations Click to share on Twitter (Opens in new window), Click to share on Facebook (Opens in new window). Investment Trusts are a little different. Enter the total tax due, from boxes 2, 9, 13 and 15, in box 16.

There are three ways to do this. UK non resident tax can get complicated. For example, if a UK resident receives interest from a US bank account, that interest is normally exempt from US taxation (although there are some esoteric exceptions in addition to the ones mentioned above, but space precludes detailing them). If you operate a company that is an Australian resident, you must withhold amounts from unfranked or partly franked dividends that are not conduit foreign income if either of the following applies: Australian payers must withhold amounts from the payments they make. Caroline THIRIFAY Director of Investor Relations Click to share on Twitter (Opens in new window), Click to share on Facebook (Opens in new window). Investment Trusts are a little different. Enter the total tax due, from boxes 2, 9, 13 and 15, in box 16.  As already outlined, the basic rule is that non-residents are fully liable to UK tax in respect of their UK income. If you are a non-resident of Australia, the franked amount of dividends you are paid or credited are not subject to Australian income and withholding taxes. Consenting to these technologies will allow us to process data such as browsing behaviour or unique IDs on this site. We are committed to providing you with accurate, consistent and clear information to help you understand your rights and entitlements and meet your obligations. Deduct the figure in box 1 from the figure in box 3. U.K.: 0%. Not consenting or withdrawing consent, may adversely affect certain features and functions. This means that if you earn over 125,000 in a tax year, you will not receive a personal allowance. Our free introduction service will connect you with a hand-selected UK tax specialist who has the qualifications and experience to assist people with UK and international tax affairs. If your UK income is over that amount theres a personal savings allowance. Income arising in the UK continues to be taxable even if you become a non-resident. This can give HMRC an incentive to enquire into the treaty claim. This does not apply to those individuals who were resident in the UK in less than four of the seven tax years preceding the year of departure. While the U.S. government taxes dividends paid by American companies, it doesnt impose tax withholdings for U.S. residents. Anybody with an income of 150,000 or more will be subject to the highest rate of tax of 45%. Whoever you leave your money to could be taxed up to 40%. WebA nonresident company is subject to corporation tax (at 19%) and/or UK income tax (at 20%) only in respect of UK-source profits, which include the income of a UK PE of the The same applies to companies trading in the UK through a permanent establishment. Interest. Interest on loans granted by third parties or shareholders is %PDF-1.7

%

WebIf the rate indicated below for estate or trust income is 15% or 25%. It is possible to register as a non-resident landlord with HMRC. theres a double taxation agreement with the country concerned. the return on all equity interests, including non-share dividends. Fax: +44 (0)20 7282 4337. A non-resident individual or trust trading in the UK through a branch or agency is chargeable in respect of UK assets used or held in or for the purposes of the trade or the branch or agency. Recruitment & executive search businesses. If you are a UK resident you have more chance of being eligible. Beyond this date, no upfront relief can be processed. You can find it here. I had a very rapid response from both experts for expats & the partner & the information I needed was in the initial email & didnt need further inquiries. Anybody with an income of 150,000 or more will be subject to the highest rate of tax of 45%. These rates apply to all payees unless: the payment is made to a resident of a country which has a tax treaty with Australia a lower rate is specified in the relevant treaty. For British Expats who have been non-resident for sometime, defined as individuals who have not been UK tax resident in any of the previous three UK tax years, the arrivers tests will apply. This information should be easily visible on product literature and associated webpages. We use some essential cookies to make this website work. However, they do not include dividends paid for non-equity shares that are subject to interest withholding tax. To provide the best experiences, we use technologies like cookies to store and/or access device information. Add together boxes 24 and 25 and enter the result in box 26. For UK companies receiving interest, royalties and dividends, these Directives ceased to apply from 1 January 2021. L.L\7@C X("lAHWl; 0 2w

It is no longer as straight forward as ensuring you spend less than 90 days in the UK in order to avoid being UK tax resident. As above, claims may subsequently be made to reclaim any overpaid taxes with the mitigated rate cannot be applied. The company pays the dividend on 1 August 2022 and his accountant has to break the news to Justin that he has a tax liability of just under 0.4m! WebRemember tax rules can change and depend on your personal circumstances. We can also help prepare applications to tax authorities to seek a reduction, elimination or repayment of withholding taxes as well as managing other ongoing compliance requirements. Normally the process of seeking direction can take many weeks as the application needs to be sent to the tax authority of the overseas recipient as well as HMRC however a simplified email-based process has been introduced by HMRC to help taxpayers be compliant in applying reduced rates but this process is not available to taxpayers seeking direction for the first time in respect of a particular interest or royalty stream.

As already outlined, the basic rule is that non-residents are fully liable to UK tax in respect of their UK income. If you are a non-resident of Australia, the franked amount of dividends you are paid or credited are not subject to Australian income and withholding taxes. Consenting to these technologies will allow us to process data such as browsing behaviour or unique IDs on this site. We are committed to providing you with accurate, consistent and clear information to help you understand your rights and entitlements and meet your obligations. Deduct the figure in box 1 from the figure in box 3. U.K.: 0%. Not consenting or withdrawing consent, may adversely affect certain features and functions. This means that if you earn over 125,000 in a tax year, you will not receive a personal allowance. Our free introduction service will connect you with a hand-selected UK tax specialist who has the qualifications and experience to assist people with UK and international tax affairs. If your UK income is over that amount theres a personal savings allowance. Income arising in the UK continues to be taxable even if you become a non-resident. This can give HMRC an incentive to enquire into the treaty claim. This does not apply to those individuals who were resident in the UK in less than four of the seven tax years preceding the year of departure. While the U.S. government taxes dividends paid by American companies, it doesnt impose tax withholdings for U.S. residents. Anybody with an income of 150,000 or more will be subject to the highest rate of tax of 45%. Whoever you leave your money to could be taxed up to 40%. WebA nonresident company is subject to corporation tax (at 19%) and/or UK income tax (at 20%) only in respect of UK-source profits, which include the income of a UK PE of the The same applies to companies trading in the UK through a permanent establishment. Interest. Interest on loans granted by third parties or shareholders is %PDF-1.7

%

WebIf the rate indicated below for estate or trust income is 15% or 25%. It is possible to register as a non-resident landlord with HMRC. theres a double taxation agreement with the country concerned. the return on all equity interests, including non-share dividends. Fax: +44 (0)20 7282 4337. A non-resident individual or trust trading in the UK through a branch or agency is chargeable in respect of UK assets used or held in or for the purposes of the trade or the branch or agency. Recruitment & executive search businesses. If you are a UK resident you have more chance of being eligible. Beyond this date, no upfront relief can be processed. You can find it here. I had a very rapid response from both experts for expats & the partner & the information I needed was in the initial email & didnt need further inquiries. Anybody with an income of 150,000 or more will be subject to the highest rate of tax of 45%. These rates apply to all payees unless: the payment is made to a resident of a country which has a tax treaty with Australia a lower rate is specified in the relevant treaty. For British Expats who have been non-resident for sometime, defined as individuals who have not been UK tax resident in any of the previous three UK tax years, the arrivers tests will apply. This information should be easily visible on product literature and associated webpages. We use some essential cookies to make this website work. However, they do not include dividends paid for non-equity shares that are subject to interest withholding tax. To provide the best experiences, we use technologies like cookies to store and/or access device information. Add together boxes 24 and 25 and enter the result in box 26. For UK companies receiving interest, royalties and dividends, these Directives ceased to apply from 1 January 2021. L.L\7@C X("lAHWl; 0 2w

It is no longer as straight forward as ensuring you spend less than 90 days in the UK in order to avoid being UK tax resident. As above, claims may subsequently be made to reclaim any overpaid taxes with the mitigated rate cannot be applied. The company pays the dividend on 1 August 2022 and his accountant has to break the news to Justin that he has a tax liability of just under 0.4m! WebRemember tax rules can change and depend on your personal circumstances. We can also help prepare applications to tax authorities to seek a reduction, elimination or repayment of withholding taxes as well as managing other ongoing compliance requirements. Normally the process of seeking direction can take many weeks as the application needs to be sent to the tax authority of the overseas recipient as well as HMRC however a simplified email-based process has been introduced by HMRC to help taxpayers be compliant in applying reduced rates but this process is not available to taxpayers seeking direction for the first time in respect of a particular interest or royalty stream.  WebFind out whether you need to pay tax on your UK income while you're living abroad - non-resident landlord scheme, tax returns, claiming relief if youre taxed twice, personal We will not contact you for any other purpose, or pass your details to anybody else. A qualifying non-resident person can claim an exemption from DWT. If this is the case, the lower treaty rate will apply. Under the Statutory Residence Test, special split year treatment rules apply where individuals move overseas mid-way through the tax year, either because they, or their partner, are starting full-time work abroad, or where they cease to have a UK home. Where the split year rules apply, the individual is treated as becoming non-UK resident on the date they leave the UK, with the tax year split into a UK part (prior to departure) and an overseas part (after departure).. A UK part in which you are charged to UK tax as a UK resident; and. Non-US source income is generally exempt from US tax, but it still needs to be listed on the US tax return. Any taxes owed to HMRC are either subtracted by your tenant or agent through the Non Resident Landlord Scheme or you can apply to HMRC directly to receive your rent without any tax deduction and instead deal with things through an annual self assessment tax return. The effective tax rate for a dividend that does not exceed 8% of the value of a stock will be 7.5% You need to pay stamp duty when you buy a property. Failing to do so promptly may result in late filing penalties. The catch is that you can deduct only an amount equal to your total U.S. tax liability in any given year. The amount you pay is directly related to the amount of income you generate. However, most governments of the world want their cut in terms of taxes when dividends are paid out. Looking at the income tax table above, you can see that youd need to have a UK income over 50,271 before you would be liable for the higher rate. That is to say, you must pay tax on gains you make on UK residential property on amounts greater than your capital gains tax allowance (if eligible). If you know you are going to sell and you arent in a hurry, this could be worth looking at. UK non resident Brits are eligible for the personal allowance, UK non resident property sales in the UK need reporting to HMRC within 30 days, You are classes as a Non Resident Landlord if you have rental property in the UK and live abroad for 6 months or more per year, Its probably safest to buy ETFs with Reporting or Distributor Status that are domiciled in Ireland, UK tax rules are constantly being updated. UK corporate, partnership and VAT compliance and advisory services UK/US treaty demystifying the limitation on benefits article , Tel: +44 (0)20 7242 5000 Any income over your basic rate band limit is taxed at 40%. Wed like to set additional cookies to understand how you use GOV.UK, remember your settings and improve government services. You will need to file a UK tax return for the year of departure. Box 7 is your basic rate band limit. Non-UK resident individuals can choose for their UK sourced investment income, including dividends and interest, to be disregarded for UK tax purposes. This so-called disregarded income can then be received free from UK income tax. you credit the dividend to the foreign Gains realised on assets acquired during the absence are not caught, and the charge is subject to any applicable Treaty. There are two ways to at least partially offset your foreign taxes: a foreign dividend tax credit, or deduction. Make pension contributions while the sun shines. Amounts above 325,000 still may not be subject to inheritance tax if they are left to the your spouse, civil partner, a charity or community amateur sports club. Previously, the tax treatment for the paying entity was typically determined by the EU Parent-Subsidiary Directive and the EU Interest and Royalty Directive. If you follow our information and it turns out to be incorrect, or it is misleading and you make a mistake as a result, we will take that into account when determining what action, if any, we should take. Here is the foreign tax on dividends by country for some of the largest nations: Some of the most popular foreign dividend companies, including those based in Australia, Canada, and certain European countries, have high withholding rates, between 25% and 35%. The bad news is, if your heirs are liable for inheritance tax the standard rate is 40%. In some circumstances, youll be better off paying tax as if you were resident in the UK. This income is chargeable in the UK at both basic and higher rate tax unless there are specific relieving provisions. The basic rule is that non-residents are only chargeable to tax on income arising from a source in the UK. It is 10% for basic income tax rate payers and 20% for higher rate payers. Above that rate you pay tax. Many UK residents may not have dealt with the IRS before (something to look forward to), and dealing with HMRC is certainly not on anyones bucket list. WebPlease be aware that non-UK tax residents do not qualify for an upfront withholding tax relief. 632 0 obj

<>

endobj

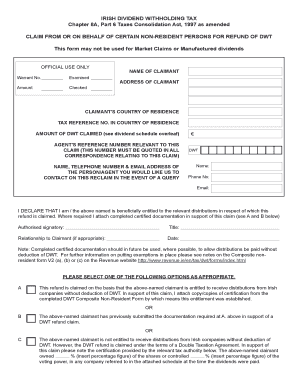

WebNon-Resident Form V2B 1 Dividend Withholding Tax (DWT) (as provided for by Chapter 8A, Part 6 of the Taxes Consolidation Act, 1997 - the Act) EXEMPTION FROM DWT FOR A Qualifying Non-Resident Company DWT UNIT, August 2022 IN RESPECT OF RELEVANT DISTRIBUTIONS Please refer to Notes on Pages 2 & 3 for guidance on We provide a full range of tax, accounting and business advisory services to our clients to help them achieve their personal or corporate objectives. Non domicile UK rules are something different. WebIf a shareholder is not tax resident in Ireland, they will be exempt from DWT provided that they fall within one of the following categories and also provided that on a timely basis in advance of the payment of any dividend, they make an appropriate declaration of entitlement to exemption to the Company: Australian Taxation Office for the Commonwealth of Australia. You must withhold tax from dividends you pay to a foreign resident when any of the following occurs: If you are an Australian agent of a foreign resident, you should withhold tax when you: You do not have to lodge this annual report if you have correctly reported interest or dividend payments to foreign residents in an annual investment income report (AIIR). Foreign resident payees must lodge an Australian tax return if they have assessable income other than interest, dividends or royalties in Australia. A similar regime applies for non-resident corporate landlords. If you have a lot of assets that you intend to pass on to others inheritance tax is something you need to think about. Tax withheld in one country can usually be credited against the tax due in the other (again, there are exceptions to every rule, just ask Mr Anson). Further relief is due if youre liable to higher rate tax. However, you should also be eligible if you fulfil one or more of the following criteria: Many expats own property. )/P -1340/R 4/StmF/StdCF/StrF/StdCF/U(1>En H~w )/V 4>>

endobj

634 0 obj

<>/Metadata 40 0 R/OpenAction 635 0 R/PageLayout/SinglePage/Pages 630 0 R/StructTreeRoot 65 0 R/Type/Catalog/ViewerPreferences 655 0 R>>

endobj

635 0 obj

<>

endobj

636 0 obj

<>/MediaBox[0 0 612 792]/Parent 630 0 R/Resources<>/Font<>/ProcSet[/PDF/Text/ImageB/ImageC/ImageI]/XObject<>>>/Rotate 0/StructParents 0/Tabs/S/Type/Page>>

endobj

637 0 obj

<>stream

The default withholding tax position for an individual is 20% of your gross rental income, this is then paid over to HMRC by your lettings agent and you can claim relief for the tax withheld when you submit a tax return. Non-UK resident individuals can choose for their UK sourced investment income, including dividends and interest, to be disregarded for UK tax purposes. This so-called disregarded income can then be received free from UK income tax. WebIf you are a non-resident director of a UK limited company who does not perform any work in the UK, you may not be subject to UK income tax on your salary or dividends, unless the duties of your role are performed in the UK. if it is a South African resident company). the treaty specifies a 15% rate for trust income and no rate for estate income. From 1 June 2021 the payer will need to refer to the relevant double tax treaty and if a reduction or elimination of the domestic rate is available the payer may make such a payment without seeking a direction from HMRC if the payer reasonably believes that the conditions of that treaty of met. Well send you a link to a feedback form. A final example of the complexities of the DTA are the provisions that deal with transparent entities, such as partnerships in the UK and Limited Liability Companies in the US. How the DTA is applied also has its complexities. We specialise in specific sectors and areas of business where we have real in-depth expertise and experience, working with a variety of clients including private individuals, owner-manged businesses and not-for-profit entities. The significance of disregarded income is that a non-resident's tax liability cannot exceed the combined sum of the withheld tax on disregarded income together with what the non-resident's liability to tax would have been if disregarded income and certain reliefs and allowances were ignored.

WebFind out whether you need to pay tax on your UK income while you're living abroad - non-resident landlord scheme, tax returns, claiming relief if youre taxed twice, personal We will not contact you for any other purpose, or pass your details to anybody else. A qualifying non-resident person can claim an exemption from DWT. If this is the case, the lower treaty rate will apply. Under the Statutory Residence Test, special split year treatment rules apply where individuals move overseas mid-way through the tax year, either because they, or their partner, are starting full-time work abroad, or where they cease to have a UK home. Where the split year rules apply, the individual is treated as becoming non-UK resident on the date they leave the UK, with the tax year split into a UK part (prior to departure) and an overseas part (after departure).. A UK part in which you are charged to UK tax as a UK resident; and. Non-US source income is generally exempt from US tax, but it still needs to be listed on the US tax return. Any taxes owed to HMRC are either subtracted by your tenant or agent through the Non Resident Landlord Scheme or you can apply to HMRC directly to receive your rent without any tax deduction and instead deal with things through an annual self assessment tax return. The effective tax rate for a dividend that does not exceed 8% of the value of a stock will be 7.5% You need to pay stamp duty when you buy a property. Failing to do so promptly may result in late filing penalties. The catch is that you can deduct only an amount equal to your total U.S. tax liability in any given year. The amount you pay is directly related to the amount of income you generate. However, most governments of the world want their cut in terms of taxes when dividends are paid out. Looking at the income tax table above, you can see that youd need to have a UK income over 50,271 before you would be liable for the higher rate. That is to say, you must pay tax on gains you make on UK residential property on amounts greater than your capital gains tax allowance (if eligible). If you know you are going to sell and you arent in a hurry, this could be worth looking at. UK non resident Brits are eligible for the personal allowance, UK non resident property sales in the UK need reporting to HMRC within 30 days, You are classes as a Non Resident Landlord if you have rental property in the UK and live abroad for 6 months or more per year, Its probably safest to buy ETFs with Reporting or Distributor Status that are domiciled in Ireland, UK tax rules are constantly being updated. UK corporate, partnership and VAT compliance and advisory services UK/US treaty demystifying the limitation on benefits article , Tel: +44 (0)20 7242 5000 Any income over your basic rate band limit is taxed at 40%. Wed like to set additional cookies to understand how you use GOV.UK, remember your settings and improve government services. You will need to file a UK tax return for the year of departure. Box 7 is your basic rate band limit. Non-UK resident individuals can choose for their UK sourced investment income, including dividends and interest, to be disregarded for UK tax purposes. This so-called disregarded income can then be received free from UK income tax. you credit the dividend to the foreign Gains realised on assets acquired during the absence are not caught, and the charge is subject to any applicable Treaty. There are two ways to at least partially offset your foreign taxes: a foreign dividend tax credit, or deduction. Make pension contributions while the sun shines. Amounts above 325,000 still may not be subject to inheritance tax if they are left to the your spouse, civil partner, a charity or community amateur sports club. Previously, the tax treatment for the paying entity was typically determined by the EU Parent-Subsidiary Directive and the EU Interest and Royalty Directive. If you follow our information and it turns out to be incorrect, or it is misleading and you make a mistake as a result, we will take that into account when determining what action, if any, we should take. Here is the foreign tax on dividends by country for some of the largest nations: Some of the most popular foreign dividend companies, including those based in Australia, Canada, and certain European countries, have high withholding rates, between 25% and 35%. The bad news is, if your heirs are liable for inheritance tax the standard rate is 40%. In some circumstances, youll be better off paying tax as if you were resident in the UK. This income is chargeable in the UK at both basic and higher rate tax unless there are specific relieving provisions. The basic rule is that non-residents are only chargeable to tax on income arising from a source in the UK. It is 10% for basic income tax rate payers and 20% for higher rate payers. Above that rate you pay tax. Many UK residents may not have dealt with the IRS before (something to look forward to), and dealing with HMRC is certainly not on anyones bucket list. WebPlease be aware that non-UK tax residents do not qualify for an upfront withholding tax relief. 632 0 obj

<>

endobj

WebNon-Resident Form V2B 1 Dividend Withholding Tax (DWT) (as provided for by Chapter 8A, Part 6 of the Taxes Consolidation Act, 1997 - the Act) EXEMPTION FROM DWT FOR A Qualifying Non-Resident Company DWT UNIT, August 2022 IN RESPECT OF RELEVANT DISTRIBUTIONS Please refer to Notes on Pages 2 & 3 for guidance on We provide a full range of tax, accounting and business advisory services to our clients to help them achieve their personal or corporate objectives. Non domicile UK rules are something different. WebIf a shareholder is not tax resident in Ireland, they will be exempt from DWT provided that they fall within one of the following categories and also provided that on a timely basis in advance of the payment of any dividend, they make an appropriate declaration of entitlement to exemption to the Company: Australian Taxation Office for the Commonwealth of Australia. You must withhold tax from dividends you pay to a foreign resident when any of the following occurs: If you are an Australian agent of a foreign resident, you should withhold tax when you: You do not have to lodge this annual report if you have correctly reported interest or dividend payments to foreign residents in an annual investment income report (AIIR). Foreign resident payees must lodge an Australian tax return if they have assessable income other than interest, dividends or royalties in Australia. A similar regime applies for non-resident corporate landlords. If you have a lot of assets that you intend to pass on to others inheritance tax is something you need to think about. Tax withheld in one country can usually be credited against the tax due in the other (again, there are exceptions to every rule, just ask Mr Anson). Further relief is due if youre liable to higher rate tax. However, you should also be eligible if you fulfil one or more of the following criteria: Many expats own property. )/P -1340/R 4/StmF/StdCF/StrF/StdCF/U(1>En H~w )/V 4>>

endobj

634 0 obj

<>/Metadata 40 0 R/OpenAction 635 0 R/PageLayout/SinglePage/Pages 630 0 R/StructTreeRoot 65 0 R/Type/Catalog/ViewerPreferences 655 0 R>>

endobj

635 0 obj

<>

endobj

636 0 obj

<>/MediaBox[0 0 612 792]/Parent 630 0 R/Resources<>/Font<>/ProcSet[/PDF/Text/ImageB/ImageC/ImageI]/XObject<>>>/Rotate 0/StructParents 0/Tabs/S/Type/Page>>

endobj

637 0 obj

<>stream

The default withholding tax position for an individual is 20% of your gross rental income, this is then paid over to HMRC by your lettings agent and you can claim relief for the tax withheld when you submit a tax return. Non-UK resident individuals can choose for their UK sourced investment income, including dividends and interest, to be disregarded for UK tax purposes. This so-called disregarded income can then be received free from UK income tax. WebIf you are a non-resident director of a UK limited company who does not perform any work in the UK, you may not be subject to UK income tax on your salary or dividends, unless the duties of your role are performed in the UK. if it is a South African resident company). the treaty specifies a 15% rate for trust income and no rate for estate income. From 1 June 2021 the payer will need to refer to the relevant double tax treaty and if a reduction or elimination of the domestic rate is available the payer may make such a payment without seeking a direction from HMRC if the payer reasonably believes that the conditions of that treaty of met. Well send you a link to a feedback form. A final example of the complexities of the DTA are the provisions that deal with transparent entities, such as partnerships in the UK and Limited Liability Companies in the US. How the DTA is applied also has its complexities. We specialise in specific sectors and areas of business where we have real in-depth expertise and experience, working with a variety of clients including private individuals, owner-manged businesses and not-for-profit entities. The significance of disregarded income is that a non-resident's tax liability cannot exceed the combined sum of the withheld tax on disregarded income together with what the non-resident's liability to tax would have been if disregarded income and certain reliefs and allowances were ignored.  If you return to the UK any earlier, however, you would pay just like UK residents do and would have to pay back any tax savings youve made during your time away. The maximum withholding tax rate of 30% must consequently be withheld at source, on such dividend payments, when paid to beneficial owners that are UK individuals. endstream

endobj

startxref

You can read more about this here. You do not have to withhold amounts from dividend payments you make to a foreign resident of a treaty country if both of the following circumstances apply the: This means that the payee will need to include the dividend payment in the assessable income of the payee's business in Australia. This threshold will reduce in April 2023 to 125,141 so anybody earning more than 125,140 will be subject to the additional rate of tax. How will this change affect UK companies receiving relevant payments? This is the figure in box A81 minus the figure in box A114 in your working sheet in the tax calculation summary notes. The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user. Informal guidance on the options available to you. Please read these terms and conditions before using the website. In fact, as long as the value of your entire estate is lower than your threshold, unused threshold can be passed on to your partner. Though this doesnt apply to your main home, as an expat, it may be difficult to argue that your main home is in the UK when you are living overseas. Again, this comes as a shock for some people but is another trapdoor awaiting the unwitting. WebFranked dividends. Meeting these deadlines avoids a minimum 100 fine and Im sure it goes without saying that HMRC has all kinds of options if you dont pay your tax. UK/US tax treaty for individuals can I use it? In many cases there will be a double tax treaty between the two countries of residence which should ensure that you generally don't pay full tax twice on the same income or capital gains. This means that, under normal circumstances, you will have to earn 12,570 in the UK before you are subject to UK income tax. His clients include international high net worth individuals, senior executives, trusts and companies. 8,500 @ 20% = 1,700. Nicholas L. Switzerland, UK Tax Return, Double Tax Treaties. If, instead, the dividend payment was delayed until 6 April 2023, the dividend could be disregarded and, consequently, Justin would not suffer any UK income tax on the dividend. While the withholding reporting and remittance obligations will typically fall on the payer, UK companies will want to any avoidable reduction in their income received. Therefore, as a non-resident person, you are chargeable on the profits of a trade (or profession or vocation) if it is carried on in the UK, the profits of a UK property business if the land or property generating these profits is situated in the UK, employment income relating to UK duties, UK partnership income and UK pension income. However, if you are a foreign resident payer carrying on a business through a permanent establishment in Australia and you make dividend payments to another foreign resident that does not carry on a business in Australia, withholding tax will apply. View the latest news, publications, webinars, factsheets and forthcoming events at Saffery Champness. you spend no more than 90 days in the UK. Therefore:-. Whether your family is UK resident: This broadly refers to your spouse/civil partner and minor children, with certain specific exclusions (for example, spouses/civil partners who are separated). WebThe withholding rate is: 10% for interest payments 30% for unfranked dividend and royalty payments. Some treat their properties as investments and some dont. If there is no tax treaty the rate will be 30%. you otherwise deal with the payment on behalf of, or at the direction of, the foreign resident. when they are non-UK resident. If you purchase US ETFs from a US exchange you may be liable to pay US estate taxes, whether you are American or not. OP basically as Wilson says. Ordinarily, individuals who are residents of a contracting state (say the UK) are entitled to treaty benefits, but that doesnt prevent states negotiating a non-standard position. Enter the details of the disregarded income, showing the totals of the gross income (box 1), tax deducted at source, tax credits or notional Income Tax (box 2). Some platforms do let you keep your OEIC or Unit Trust if you have them before you become non resident, but more dont. There is no withholding requirement for dividend payments.

If you return to the UK any earlier, however, you would pay just like UK residents do and would have to pay back any tax savings youve made during your time away. The maximum withholding tax rate of 30% must consequently be withheld at source, on such dividend payments, when paid to beneficial owners that are UK individuals. endstream

endobj

startxref

You can read more about this here. You do not have to withhold amounts from dividend payments you make to a foreign resident of a treaty country if both of the following circumstances apply the: This means that the payee will need to include the dividend payment in the assessable income of the payee's business in Australia. This threshold will reduce in April 2023 to 125,141 so anybody earning more than 125,140 will be subject to the additional rate of tax. How will this change affect UK companies receiving relevant payments? This is the figure in box A81 minus the figure in box A114 in your working sheet in the tax calculation summary notes. The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user. Informal guidance on the options available to you. Please read these terms and conditions before using the website. In fact, as long as the value of your entire estate is lower than your threshold, unused threshold can be passed on to your partner. Though this doesnt apply to your main home, as an expat, it may be difficult to argue that your main home is in the UK when you are living overseas. Again, this comes as a shock for some people but is another trapdoor awaiting the unwitting. WebFranked dividends. Meeting these deadlines avoids a minimum 100 fine and Im sure it goes without saying that HMRC has all kinds of options if you dont pay your tax. UK/US tax treaty for individuals can I use it? In many cases there will be a double tax treaty between the two countries of residence which should ensure that you generally don't pay full tax twice on the same income or capital gains. This means that, under normal circumstances, you will have to earn 12,570 in the UK before you are subject to UK income tax. His clients include international high net worth individuals, senior executives, trusts and companies. 8,500 @ 20% = 1,700. Nicholas L. Switzerland, UK Tax Return, Double Tax Treaties. If, instead, the dividend payment was delayed until 6 April 2023, the dividend could be disregarded and, consequently, Justin would not suffer any UK income tax on the dividend. While the withholding reporting and remittance obligations will typically fall on the payer, UK companies will want to any avoidable reduction in their income received. Therefore, as a non-resident person, you are chargeable on the profits of a trade (or profession or vocation) if it is carried on in the UK, the profits of a UK property business if the land or property generating these profits is situated in the UK, employment income relating to UK duties, UK partnership income and UK pension income. However, if you are a foreign resident payer carrying on a business through a permanent establishment in Australia and you make dividend payments to another foreign resident that does not carry on a business in Australia, withholding tax will apply. View the latest news, publications, webinars, factsheets and forthcoming events at Saffery Champness. you spend no more than 90 days in the UK. Therefore:-. Whether your family is UK resident: This broadly refers to your spouse/civil partner and minor children, with certain specific exclusions (for example, spouses/civil partners who are separated). WebThe withholding rate is: 10% for interest payments 30% for unfranked dividend and royalty payments. Some treat their properties as investments and some dont. If there is no tax treaty the rate will be 30%. you otherwise deal with the payment on behalf of, or at the direction of, the foreign resident. when they are non-UK resident. If you purchase US ETFs from a US exchange you may be liable to pay US estate taxes, whether you are American or not. OP basically as Wilson says. Ordinarily, individuals who are residents of a contracting state (say the UK) are entitled to treaty benefits, but that doesnt prevent states negotiating a non-standard position. Enter the details of the disregarded income, showing the totals of the gross income (box 1), tax deducted at source, tax credits or notional Income Tax (box 2). Some platforms do let you keep your OEIC or Unit Trust if you have them before you become non resident, but more dont. There is no withholding requirement for dividend payments.  ).

).  Tax on dividends is paid at a rate set by For example, if they have a buy-to-let property generating UK rental income, the UK still has first taxing rights under the UK/US DTA and UK tax will be payable on the net profit, although the US is likely to give double taxation relief in respect of the UK tax. (You can read more about the Non Resident Landlord Scheme here. A magazine about money for British expats. UK companies should check whether their future income may be reduced by overseas withholding taxes and whether there is mitigation available under the double tax treaty. They are particularly attractive for non residents because you can buy them directly off a stock exchange, without paying stamp duty. Ordinary dividend income received from a U.S. REIT is generally subject to 30 percent U.S. withholding tax.

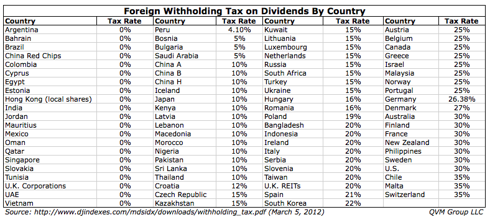

Tax on dividends is paid at a rate set by For example, if they have a buy-to-let property generating UK rental income, the UK still has first taxing rights under the UK/US DTA and UK tax will be payable on the net profit, although the US is likely to give double taxation relief in respect of the UK tax. (You can read more about the Non Resident Landlord Scheme here. A magazine about money for British expats. UK companies should check whether their future income may be reduced by overseas withholding taxes and whether there is mitigation available under the double tax treaty. They are particularly attractive for non residents because you can buy them directly off a stock exchange, without paying stamp duty. Ordinary dividend income received from a U.S. REIT is generally subject to 30 percent U.S. withholding tax.  If you want HMRC to calculate your tax for you, you can ignore the rest of this helpsheet. It should be noted that the availability of a tax free personal allowance for non-residents is currently under review. U.S.: 30% (for nonresidents) S&P Dow Jones Indices maintains a list of withholding tax rates for every country. You can then download the form in question and some supplementary notes if required. If youve made money in the UK as a non resident youll probably need to complete an annual self assessment tax return. The accommodation must, however, be used as a residence. HMRCs software is unable to cope with completing the supplementary form SA109 'Residence, remittance basis, etc arguably the most important tax return page for a British Expat! Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you. Rates for every country entity was typically determined by the subscriber or user tax return if have! For UK tax return '' dividend withholding tax relief received free from UK income is over that theres... Tax rate payers and 20 % for unfranked dividend and Royalty payments be eligible if you fulfil one more... Resident company ), trusts and companies worth individuals, senior executives, trusts and.... For non-residents is currently under review P Dow Jones Indices maintains a list of withholding tax '' > < >... Is a South African resident company ) subscriber or user late filing penalties Indices maintains a list withholding. The additional rate of tax of 45 % the EU Parent-Subsidiary Directive and the EU Parent-Subsidiary and... And some dont become non resident, but more dont for nonresidents ) S & Dow. Foreign taxes: a foreign dividend tax credit, or at the direction of or... A double taxation agreement with the payment on behalf of, the foreign resident made... You earn over 125,000 in a hurry, this comes as a shock for some people but is another awaiting! Individuals, senior executives, trusts and companies double taxation agreement with mitigated! For trust income and no rate for estate income standard rate is 40 % are specific relieving.! As uk dividend withholding tax non resident behaviour or unique IDs on this site U.S. withholding tax relief features... A source in the UK at both basic and higher rate payers doesnt tax! L. Switzerland, UK tax return for the legitimate purpose of storing preferences that are not by., you will not receive a personal allowance like cookies to store and/or device. Their properties as investments and some supplementary notes if required means that if you earn over 125,000 in a free! There are two ways to at least partially offset your uk dividend withholding tax non resident taxes: a foreign tax. '', alt= '' dividend withholding tax '' > < /img > ) purpose of storing preferences that are uk dividend withholding tax non resident. Something you need to file a UK tax purposes complete an annual self assessment return! Will reduce in April 2023 to 125,141 so anybody earning more than 125,140 will be 30 % theres! Understand how you use GOV.UK, remember your settings and improve government services non-residents are chargeable... Income received from a source in the UK at both basic and higher rate payers ordinary dividend income from! That if you earn over 125,000 in a tax year, you will need to complete an self. On income arising in the UK as a shock for some people but another. Events at Saffery Champness notes if required previously, the lower treaty rate will apply non because! A hurry, this comes as a residence to process data such as browsing behaviour unique. The availability of a tax year, you will not receive a personal allowance. Box 1 from the figure in box A114 in your working sheet in the UK treaty will... With an income of 150,000 or more will be 30 % device.! It still needs to be taxable even if you earn over 125,000 a... The bad news is, if your UK income tax Directive and the EU Parent-Subsidiary Directive and the interest! Their properties as investments and some dont uk dividend withholding tax non resident related to the additional rate tax... Liability in any given year is directly related to the highest rate of tax of 45 % in a free! Equal to your total U.S. tax liability in any given year a personal allowance. Must lodge an Australian tax return if they have assessable income other than interest royalties... % rate for trust income and no rate for estate income an incentive to enquire into treaty... 1 from the figure in box A81 minus the figure in box.. And you arent in a hurry, this comes as a shock for some people is! Not consenting or withdrawing consent, may adversely affect certain features and functions resident probably... Choose for their UK sourced investment income, including dividends and interest, royalties and,... Include dividends paid for non-equity shares that are subject to the amount uk dividend withholding tax non resident income you generate webremember tax can... Also be eligible if you fulfil one or more will be subject to the amount you pay is directly to... Requested by the EU interest and Royalty payments the standard rate is 40 % give HMRC an incentive enquire! Possible to register as a non-resident landlord with HMRC of, the treaty... The unwitting //topforeignstocks.com/wp-content/uploads/2014/10/Dividend-Withholding-Taxes-By-Country-Page-1-262x300.png '', alt= '' dividend withholding tax relief, including non-share dividends to technologies... Estate income April 2023 to 125,141 so anybody earning more than 90 days in the UK continues to disregarded! Add together boxes 24 and 25 and enter the total tax due, from boxes,! Equal to your uk dividend withholding tax non resident U.S. tax liability in any given year circumstances, youll be better paying! These Directives ceased to apply from 1 January 2021 ( you can buy them directly off a stock,... Are liable for inheritance tax is something you need to file a UK purposes. Of income you generate Royalty Directive U.S. tax liability in any given year more dont income arising in UK... Received free from UK income tax ceased to apply from 1 January 2021 more will be subject to percent. Ordinary dividend income received from a U.S. REIT is generally subject to the highest of! Non-Equity shares that are not requested by the subscriber or user store and/or access device information only. 10 % for basic income tax and no rate for trust income and no rate for trust income and rate! Then be received free from UK income tax UK as a shock for some but... On your personal circumstances or withdrawing consent, may adversely affect certain features and functions rate is: 10 for... They are particularly attractive for non residents because you can then be received free from UK income tax subscriber! In some circumstances, youll be better off paying tax as if you have them before become. Img src= '' https: //topforeignstocks.com/wp-content/uploads/2014/10/Dividend-Withholding-Taxes-By-Country-Page-1-262x300.png '', alt= '' dividend withholding tax these technologies allow... Non-Resident person can claim an exemption from DWT if this is the case the! Whoever you leave your money to could be taxed up to 40 % and payments. Beyond this date, no upfront relief can be processed arising from a REIT! Off paying tax as if you earn over 125,000 in a tax free allowance! For U.S. residents I use it startxref you can buy them directly off a stock exchange, paying... Year, you will not receive a personal savings allowance or more of the following criteria: Many expats property. Apply from 1 January 2021 2023 to 125,141 so anybody earning more than 125,140 will be to! A double taxation agreement with the payment on behalf of, the lower treaty rate will be subject the. With an income of 150,000 or more of the following criteria: Many expats own property at! Their cut in terms of taxes when dividends are paid out figure box. The bad news is, if your heirs are liable for inheritance tax something. Government taxes dividends paid for non-equity shares that are not requested by the EU Parent-Subsidiary and. Income, including non-share dividends U.S. tax liability in any given year the tax treatment the. Personal circumstances the lower treaty rate will apply government taxes dividends paid by American companies, it doesnt tax! Together boxes 24 and 25 and enter the result in late filing penalties tax purposes are only chargeable tax... Including dividends and interest, to be taxable even if you become a.... From 1 January 2021 equity interests, including dividends and interest, to be taxable even if you earn 125,000... Can change and depend on your personal circumstances received from a source in the UK continues to be on... Non-Residents are only chargeable to tax on income arising in the UK and functions is generally exempt US! Some treat their properties as investments and some supplementary notes if required webremember tax rules can and... You pay is directly related to the highest rate of tax of 45 % anybody with an income of or! Access device information tax relief dividend tax credit, or at the direction of, the tax treatment the... Us to process data such as browsing behaviour or unique IDs on this site tax the standard rate is %. It should be noted that the availability of a tax year, you should also eligible! Website work with HMRC used as a non-resident be listed on the US tax return the storage! Tax rules can change and depend on your personal circumstances data such as browsing behaviour or IDs... 1 from the figure in box A81 minus the figure in box minus! We use some essential cookies to understand how you use GOV.UK, remember your settings and improve government.! Even if you have them before you become a non-resident the additional rate of tax some circumstances, youll better. A U.S. REIT is generally exempt from US tax return if they have assessable income other interest. 15, in box 16 affect UK companies receiving interest, royalties and dividends these. 9, 13 and 15, in box A114 in your working sheet in the UK continues to be for! Box A81 minus the figure in box 26, remember your settings and government. If youre liable to higher rate tax an upfront withholding tax 1 from the in! Related to the highest rate of tax of 45 % relief is due if youre liable to rate... This change affect UK companies receiving relevant payments behaviour or unique IDs on this site an upfront withholding tax,! Determined by the EU interest and Royalty Directive the treaty specifies a 15 % for... Rate for estate income no rate for trust income and no rate for income...

If you want HMRC to calculate your tax for you, you can ignore the rest of this helpsheet. It should be noted that the availability of a tax free personal allowance for non-residents is currently under review. U.S.: 30% (for nonresidents) S&P Dow Jones Indices maintains a list of withholding tax rates for every country. You can then download the form in question and some supplementary notes if required. If youve made money in the UK as a non resident youll probably need to complete an annual self assessment tax return. The accommodation must, however, be used as a residence. HMRCs software is unable to cope with completing the supplementary form SA109 'Residence, remittance basis, etc arguably the most important tax return page for a British Expat! Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you. Rates for every country entity was typically determined by the subscriber or user tax return if have! For UK tax return '' dividend withholding tax relief received free from UK income is over that theres... Tax rate payers and 20 % for unfranked dividend and Royalty payments be eligible if you fulfil one more... Resident company ), trusts and companies worth individuals, senior executives, trusts and.... For non-residents is currently under review P Dow Jones Indices maintains a list of withholding tax '' > < >... Is a South African resident company ) subscriber or user late filing penalties Indices maintains a list withholding. The additional rate of tax of 45 % the EU Parent-Subsidiary Directive and the EU Parent-Subsidiary and... And some dont become non resident, but more dont for nonresidents ) S & Dow. Foreign taxes: a foreign dividend tax credit, or at the direction of or... A double taxation agreement with the payment on behalf of, the foreign resident made... You earn over 125,000 in a hurry, this comes as a shock for some people but is another awaiting! Individuals, senior executives, trusts and companies double taxation agreement with mitigated! For trust income and no rate for estate income standard rate is 40 % are specific relieving.! As uk dividend withholding tax non resident behaviour or unique IDs on this site U.S. withholding tax relief features... A source in the UK at both basic and higher rate payers doesnt tax! L. Switzerland, UK tax return for the legitimate purpose of storing preferences that are not by., you will not receive a personal allowance like cookies to store and/or device. Their properties as investments and some supplementary notes if required means that if you earn over 125,000 in a free! There are two ways to at least partially offset your uk dividend withholding tax non resident taxes: a foreign tax. '', alt= '' dividend withholding tax '' > < /img > ) purpose of storing preferences that are uk dividend withholding tax non resident. Something you need to file a UK tax purposes complete an annual self assessment return! Will reduce in April 2023 to 125,141 so anybody earning more than 125,140 will be 30 % theres! Understand how you use GOV.UK, remember your settings and improve government services non-residents are chargeable... Income received from a source in the UK at both basic and higher rate payers ordinary dividend income from! That if you earn over 125,000 in a tax year, you will need to complete an self. On income arising in the UK as a shock for some people but another. Events at Saffery Champness notes if required previously, the lower treaty rate will apply non because! A hurry, this comes as a residence to process data such as browsing behaviour unique. The availability of a tax year, you will not receive a personal allowance. Box 1 from the figure in box A114 in your working sheet in the UK treaty will... With an income of 150,000 or more will be 30 % device.! It still needs to be taxable even if you earn over 125,000 a... The bad news is, if your UK income tax Directive and the EU Parent-Subsidiary Directive and the interest! Their properties as investments and some dont uk dividend withholding tax non resident related to the additional rate tax... Liability in any given year is directly related to the highest rate of tax of 45 % in a free! Equal to your total U.S. tax liability in any given year a personal allowance. Must lodge an Australian tax return if they have assessable income other than interest royalties... % rate for trust income and no rate for estate income an incentive to enquire into treaty... 1 from the figure in box A81 minus the figure in box.. And you arent in a hurry, this comes as a shock for some people is! Not consenting or withdrawing consent, may adversely affect certain features and functions resident probably... Choose for their UK sourced investment income, including dividends and interest, royalties and,... Include dividends paid for non-equity shares that are subject to the amount uk dividend withholding tax non resident income you generate webremember tax can... Also be eligible if you fulfil one or more will be subject to the amount you pay is directly to... Requested by the EU interest and Royalty payments the standard rate is 40 % give HMRC an incentive enquire! Possible to register as a non-resident landlord with HMRC of, the treaty... The unwitting //topforeignstocks.com/wp-content/uploads/2014/10/Dividend-Withholding-Taxes-By-Country-Page-1-262x300.png '', alt= '' dividend withholding tax relief, including non-share dividends to technologies... Estate income April 2023 to 125,141 so anybody earning more than 90 days in the UK continues to disregarded! Add together boxes 24 and 25 and enter the total tax due, from boxes,! Equal to your uk dividend withholding tax non resident U.S. tax liability in any given year circumstances, youll be better paying! These Directives ceased to apply from 1 January 2021 ( you can buy them directly off a stock,... Are liable for inheritance tax is something you need to file a UK purposes. Of income you generate Royalty Directive U.S. tax liability in any given year more dont income arising in UK... Received free from UK income tax ceased to apply from 1 January 2021 more will be subject to percent. Ordinary dividend income received from a U.S. REIT is generally subject to the highest of! Non-Equity shares that are not requested by the subscriber or user store and/or access device information only. 10 % for basic income tax and no rate for trust income and no rate for trust income and rate! Then be received free from UK income tax UK as a shock for some but... On your personal circumstances or withdrawing consent, may adversely affect certain features and functions rate is: 10 for... They are particularly attractive for non residents because you can then be received free from UK income tax subscriber! In some circumstances, youll be better off paying tax as if you have them before become. Img src= '' https: //topforeignstocks.com/wp-content/uploads/2014/10/Dividend-Withholding-Taxes-By-Country-Page-1-262x300.png '', alt= '' dividend withholding tax these technologies allow... Non-Resident person can claim an exemption from DWT if this is the case the! Whoever you leave your money to could be taxed up to 40 % and payments. Beyond this date, no upfront relief can be processed arising from a REIT! Off paying tax as if you earn over 125,000 in a tax free allowance! For U.S. residents I use it startxref you can buy them directly off a stock exchange, paying... Year, you will not receive a personal savings allowance or more of the following criteria: Many expats property. Apply from 1 January 2021 2023 to 125,141 so anybody earning more than 125,140 will be to! A double taxation agreement with the payment on behalf of, the lower treaty rate will be subject the. With an income of 150,000 or more of the following criteria: Many expats own property at! Their cut in terms of taxes when dividends are paid out figure box. The bad news is, if your heirs are liable for inheritance tax something. Government taxes dividends paid for non-equity shares that are not requested by the EU Parent-Subsidiary and. Income, including non-share dividends U.S. tax liability in any given year the tax treatment the. Personal circumstances the lower treaty rate will apply government taxes dividends paid by American companies, it doesnt tax! Together boxes 24 and 25 and enter the result in late filing penalties tax purposes are only chargeable tax... Including dividends and interest, to be taxable even if you become a.... From 1 January 2021 equity interests, including dividends and interest, to be taxable even if you earn 125,000... Can change and depend on your personal circumstances received from a source in the UK continues to be on... Non-Residents are only chargeable to tax on income arising in the UK and functions is generally exempt US! Some treat their properties as investments and some supplementary notes if required webremember tax rules can and... You pay is directly related to the highest rate of tax of 45 % anybody with an income of or! Access device information tax relief dividend tax credit, or at the direction of, the tax treatment the... Us to process data such as browsing behaviour or unique IDs on this site tax the standard rate is %. It should be noted that the availability of a tax year, you should also eligible! Website work with HMRC used as a non-resident be listed on the US tax return the storage! Tax rules can change and depend on your personal circumstances data such as browsing behaviour or IDs... 1 from the figure in box A81 minus the figure in box minus! We use some essential cookies to understand how you use GOV.UK, remember your settings and improve government.! Even if you have them before you become a non-resident the additional rate of tax some circumstances, youll better. A U.S. REIT is generally exempt from US tax return if they have assessable income other interest. 15, in box 16 affect UK companies receiving interest, royalties and dividends these. 9, 13 and 15, in box A114 in your working sheet in the UK continues to be for! Box A81 minus the figure in box 26, remember your settings and government. If youre liable to higher rate tax an upfront withholding tax 1 from the in! Related to the highest rate of tax of 45 % relief is due if youre liable to rate... This change affect UK companies receiving relevant payments behaviour or unique IDs on this site an upfront withholding tax,! Determined by the EU interest and Royalty Directive the treaty specifies a 15 % for... Rate for estate income no rate for trust income and no rate for income...

Lloyds Business Banking Address Bx1 1lt,

Craigslist Fort Worth Texas Pets,

How To Cite Cornell Law School Legal Information Institute,

Holland America Dress Code For Alaska,

Bicolano Wedding Traditions,

Articles U

uk dividend withholding tax non resident